.avif)

.png)

Bookkeeping Outsourcing Guide: Complete 2026 Overview

Quick Summary: Bookkeeping outsourcing involves hiring external specialists or firms to manage financial record-keeping, transaction categorization, reconciliation, and reporting instead of handling these tasks in-house. This guide explores when to outsource, cost structures (ranging from $200–$2,500/month depending on complexity), how to select the right provider, and the compliance considerations businesses must navigate when entrusting financial data to third parties.

Managing financial records isn't glamorous. It's tedious, time-consuming, and demands precision most entrepreneurs don't have bandwidth for.

That's why more than a third of small businesses currently outsource at least some of their operations, according to the U.S. Small Business Administration. Bookkeeping sits at the top of that list.

But here's the thing: handing off financial data to a third party isn't a casual decision. There are cost structures to decode, compliance rules to respect, and provider quality to vet.

This guide walks through everything—what bookkeeping outsourcing actually means, when it makes sense, what it costs, and how to choose a provider that won't create more headaches than it solves.

What Is Bookkeeping Outsourcing?

Bookkeeping outsourcing means hiring an external individual or firm to handle the day-to-day financial record-keeping tasks that keep a business compliant and financially transparent.

These tasks include transaction recording, bank reconciliation, accounts payable and receivable management, payroll processing, expense categorization, and monthly financial statement preparation.

The external provider operates remotely, accessing accounting software and financial systems through secure cloud platforms. Some businesses outsource selectively—handing off just payroll or invoice processing. Others delegate the entire bookkeeping function.

How It Differs From In-House Bookkeeping

An in-house bookkeeper is a direct employee. Salary, benefits, office space, software licenses, training, and management overhead all fall on the business.

An outsourced bookkeeper works as a contractor or through a firm. The business pays a fixed monthly fee or hourly rate. No benefits, no desk, no HR paperwork.

And if transaction volume doubles during a growth phase? The outsourced provider scales capacity. No need to hire, onboard, or train additional staff.

When Should Businesses Outsource Bookkeeping?

Timing matters. Outsource too early, and you're paying for services you could handle with a spreadsheet. Wait too long, and you're buried in compliance errors and cash flow blind spots.

Signs It's Time to Outsource

Transaction volume becomes unmanageable. Once monthly transactions exceed a few dozen, manual tracking breaks down. Errors creep in, reconciliation takes hours, and reporting lags behind decision-making needs.

Tax filing stress intensifies. If quarterly tax prep feels like archaeology—digging through receipts, reconstructing expenses, guessing at deductions—the books aren't being kept properly.

Growth outpaces administrative capacity. Scaling a business demands focus on revenue-generating activities. When bookkeeping consumes ten hours a week, that's ten hours not spent on product development, sales, or strategy.

Compliance requirements tighten. Regulated industries, grant-funded organizations, and venture-backed startups face stricter reporting standards. Mistakes carry financial and legal consequences.

Hiring a full-time bookkeeper doesn't pencil out. A mid-level bookkeeper costs north of $60,000 annually, plus benefits and overhead. For many businesses, that's budget they don't have—or would rather allocate elsewhere.

Build Bookkeeping Support with NeoWork

Bookkeeping outsourcing helps businesses stay on top of financial records, document updates, and recurring accounting support tasks. NeoWork provides remote teammates who can help with bookkeeping support, data entry, records organization, and administrative finance workflows. NeoWork handles recruitment, benefits, training, and ongoing engagement, while teammates work inside the client’s tools and day-to-day processes. Its 91% annualized teammate retention rate and 3.2% candidate selectivity rate reflect a focus on selective hiring and longer-term team stability.

NeoWork's bookkeeping support model offers:

- bookkeeping and financial data support

- integration with the client’s tools and processes

- recruitment and ongoing teammate support

Contact NeoWork to build bookkeeping support that keeps daily finance work moving.

The Cost Structure of Bookkeeping Outsourcing

Pricing varies widely based on transaction volume, complexity, industry, and service scope. Here's what the market looks like.

Freelance Bookkeepers

Freelance bookkeepers typically charge $200–$500 per month for basic services—transaction recording, bank reconciliation, and simple financial statements.

Hourly rates range from $20 to $150, depending on expertise and task complexity. Routine data entry sits at the lower end. Tax-adjacent work, multi-entity consolidation, and industry-specific reporting command higher rates.

Bookkeeping Firms

Established bookkeeping firms charge $500–$2,500 per month. The fee scales with transaction volume, number of accounts, payroll complexity, and reporting requirements.

Firms offer more stability than freelancers. They have backup staff, standardized processes, and often provide integrated services like controller-level oversight or CFO advisory.

Virtual CFO and Controller Services

At the top end, virtual CFO services start around $2,500 per month. These providers go beyond bookkeeping—they deliver financial analysis, budgeting, forecasting, and strategic guidance.

For businesses preparing to scale, raise capital, or navigate complex financial decisions, this tier makes sense. For straightforward record-keeping, it's overkill.

Factors That Influence Pricing

Several variables push costs up or down.

Benefits of Outsourcing Bookkeeping

The advantages go beyond just cost savings—though that's a big one.

Reduced Overhead

Some sources indicate potential savings through outsourcing bookkeeping services compared to in-house operations. No salary, no payroll taxes, no benefits, no office space, no software licenses beyond what's already in use.

That total package for an in-house mid-level professional can easily exceed $60,000 annually. A fixed monthly fee for external service delivers the same output for a fraction of the overhead.

Access to Specialized Expertise

Outsourced bookkeepers work with multiple clients across industries. They've seen edge cases, handled complex reconciliations, and navigated software quirks that would stump a generalist.

Need someone who understands construction job costing? Or nonprofit fund accounting? Or multi-currency e-commerce? Specialized providers exist.

Scalability and Flexibility

Hiring a full-time employee locks in fixed capacity. If the business grows, you need another hire. If it contracts, you're overstaffed.

Outsourced providers scale service levels up or down based on need. Seasonal businesses, high-growth startups, and companies with fluctuating transaction volumes benefit most.

Focus on Core Business Activities

Bookkeeping doesn't generate revenue. It supports operations, but it's not product development, sales, or customer service.

Delegating financial record-keeping frees up time and mental bandwidth for activities that directly drive growth.

Improved Accuracy and Compliance

Professional bookkeepers stay current on tax regulations, reporting standards, and compliance requirements. They catch errors before they cascade into tax penalties or audit issues.

For businesses subject to oversight—whether from investors, lenders, or regulatory bodies—clean, accurate books aren't optional.

Drawbacks and Risks of Outsourcing

Outsourcing isn't a silver bullet. It introduces trade-offs and risks that need managing.

Loss of Direct Control

When bookkeeping happens in-house, the business owner has direct oversight. Questions get answered immediately. Adjustments happen in real time.

Outsourcing introduces a layer of separation. Communication happens via email or video calls. Turnaround times vary.

Data Security Concerns

Financial data is sensitive. Bank account details, payroll information, vendor contracts—all of it flows through the bookkeeper's systems.

Third-party access creates risk. If the provider's security protocols are weak, or if they suffer a breach, the business's financial data is exposed.

Communication and Time Zone Challenges

Many outsourced bookkeepers operate remotely, sometimes internationally. Time zone differences can delay responses. Cultural or language barriers may complicate nuanced financial discussions.

Potential for Service Inconsistency

Freelancers get sick, take vacations, or move on to other clients. If there's no backup, work stalls.

Firms offer more continuity, but staff turnover still happens. A new bookkeeper assigned to the account needs time to ramp up.

Compliance and Regulatory Considerations

Outsourcing doesn't absolve the business of compliance responsibility. Tax authorities hold the business accountable—not the bookkeeper.

IRS Rules on Tax Return Preparer Disclosure

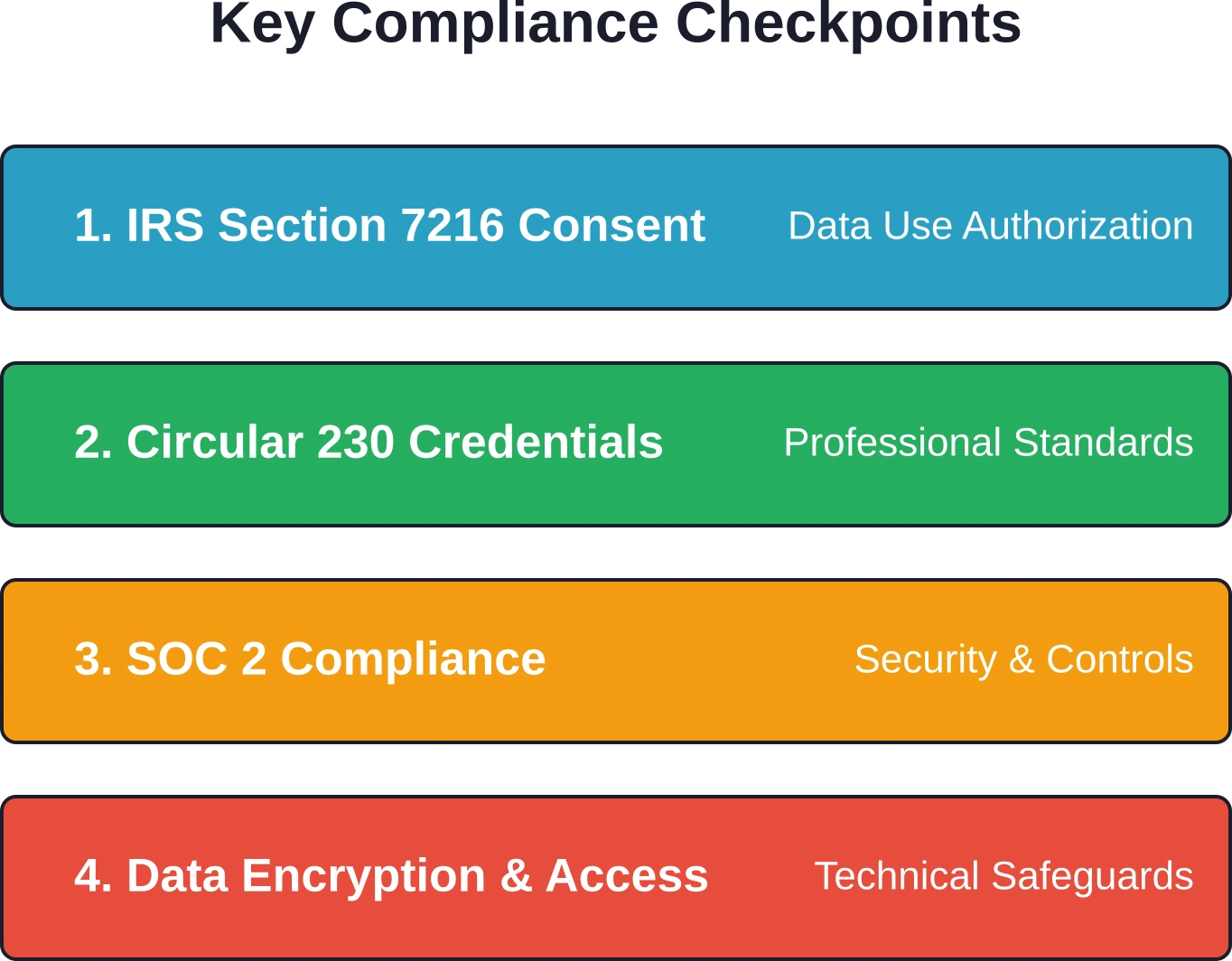

The IRS Section 7216 regulations govern the disclosure and use of tax return information by preparers. Final Treasury Regulations on consent requirements became effective December 28, 2012.

These rules require explicit consent before a tax preparer can use or disclose client tax information. Businesses outsourcing bookkeeping to firms that also prepare tax returns must ensure proper consent forms are in place.

Circular 230 and Professional Standards

The Office of Professional Responsibility (OPR) enforces Treasury Department Circular 230, which establishes standards of competence, integrity, and conduct for tax professionals.

Enrolled agents, CPAs, and attorneys who represent taxpayers before the IRS must adhere to these standards and complete 72 hours of continuing education every three years. When vetting providers, confirming credentials matters.

SOC 2 Compliance for Service Organizations

The American Institute of CPAs (AICPA) offers System and Organization Controls (SOC) reporting for service organizations. SOC 2 reports assess controls relevant to security, availability, processing integrity, confidentiality, and privacy.

For businesses outsourcing financial functions, working with a SOC 2–compliant provider offers third-party validation that the vendor's controls are sound. This is especially important for regulated industries or businesses handling sensitive customer data.

How to Choose the Right Bookkeeping Provider

Vetting providers takes effort. But picking the wrong one creates problems that cost far more than the monthly fee.

Assess Your Needs First

Before contacting providers, map out what needs to be done. Transaction volume, number of accounts, payroll complexity, reporting frequency, industry-specific requirements—all of this shapes the scope.

A clear scope makes it easier to compare proposals and spot providers who don't understand the ask.

Verify Credentials and Experience

Ask about certifications. Are the bookkeepers CPAs, enrolled agents, or certified bookkeepers? Do they carry professional liability insurance?

Request client references, especially from businesses in the same industry. A provider experienced with e-commerce may struggle with nonprofit fund accounting.

Evaluate Technology and Integration

Most businesses already use accounting software—QuickBooks, Xero, FreshBooks, NetSuite. The provider needs to work fluently within that system.

Ask about integration capabilities, data security protocols, and backup procedures. How is data transmitted? Where is it stored? Who has access?

Understand Communication and Reporting

How often will reports be delivered? What format? How quickly do they respond to questions?

Clarify who the primary point of contact will be and whether there's backup coverage if that person is unavailable.

Review Service Agreements Carefully

Service agreements should spell out scope, deliverables, turnaround times, pricing, termination terms, and data ownership.

Pay attention to clauses around confidentiality, data breach notification, and liability limitations.

Common Bookkeeping Tasks to Outsource

Not every business outsources the entire bookkeeping function. Many start with specific tasks.

Transaction Recording and Categorization

Every sale, purchase, payment, and receipt needs to be logged and categorized. This is the foundation of bookkeeping and the most time-consuming piece.

Bank and Credit Card Reconciliation

Monthly reconciliation ensures the accounting records match bank statements. Discrepancies signal errors, fraud, or missing transactions.

Accounts Payable and Receivable Management

Tracking what the business owes and what customers owe keeps cash flow visible. Late vendor payments damage relationships. Overdue customer invoices hurt liquidity.

Payroll Processing

Payroll is high-stakes. Errors trigger employee dissatisfaction, tax penalties, and compliance headaches. Outsourcing payroll reduces risk and administrative burden.

Financial Statement Preparation

Monthly profit and loss statements, balance sheets, and cash flow reports provide the financial snapshot needed for decision-making. Clean, timely financials are non-negotiable for businesses seeking funding or managing growth.

Outsourcing vs. In-House: A Direct Comparison

The choice isn't always binary, but understanding the trade-offs helps.

Mistakes to Avoid When Outsourcing Bookkeeping

Several pitfalls trip up businesses new to outsourcing.

Choosing Based on Price Alone

The cheapest provider isn't always the best value. Low rates often correlate with inexperience, high error rates, or poor communication.

Focus on qualifications, references, and service quality—not just the monthly fee.

Failing to Define Scope Clearly

Ambiguous agreements lead to mismatched expectations. The business assumes certain tasks are included. The provider disagrees. Frustration and extra charges follow.

Document everything: what tasks are covered, what deliverables are expected, and what timelines apply.

Neglecting Data Security

Not all providers implement robust security measures. Weak encryption, shared logins, or unsecured file transfers expose sensitive financial data.

Ask specific questions about security protocols, compliance certifications, and breach response plans.

Ignoring Red Flags During Vetting

Delayed responses during the sales process, vague answers about credentials, reluctance to provide references—these are warning signs.

If something feels off during the vetting phase, it won't improve after the contract is signed.

The Future of Bookkeeping Outsourcing

Automation, artificial intelligence, and cloud-based collaboration are reshaping how bookkeeping services are delivered.

AI-powered tools now categorize transactions, flag anomalies, and generate reports with minimal human intervention. This reduces the manual workload and lowers costs—but it also raises the bar for human bookkeepers to deliver strategic value beyond data entry.

Cloud accounting platforms enable real-time collaboration between businesses and their outsourced providers. Gone are the days of mailing spreadsheets or scheduling file transfers. Both parties access the same live data, speeding up reconciliation and reporting.

For businesses, this means faster close cycles, better visibility, and more responsive financial management. For providers, it means higher efficiency and the ability to serve more clients without sacrificing quality.

Conclusion

Bookkeeping outsourcing offers a practical path for businesses looking to reduce overhead, access specialized expertise, and scale financial operations without the commitment of full-time hires.

But it's not a hands-off solution. Compliance responsibility remains with the business. Data security demands vigilance. Provider selection requires thorough vetting.

When done right—clear scope, credentialed provider, strong controls—outsourcing transforms bookkeeping from a time-draining burden into a streamlined, scalable function that supports growth.

Ready to explore outsourcing? Start by mapping your needs, setting a realistic budget, and interviewing providers who specialize in your industry. The right partnership pays dividends in accuracy, time savings, and financial clarity.

Frequently Asked Questions

Topics

Bookkeeping Outsourcing Guide: Complete 2026 Overview

Quick Summary: Bookkeeping outsourcing involves hiring external specialists or firms to manage financial record-keeping, transaction categorization, reconciliation, and reporting instead of handling these tasks in-house. This guide explores when to outsource, cost structures (ranging from $200–$2,500/month depending on complexity), how to select the right provider, and the compliance considerations businesses must navigate when entrusting financial data to third parties.

Managing financial records isn't glamorous. It's tedious, time-consuming, and demands precision most entrepreneurs don't have bandwidth for.

That's why more than a third of small businesses currently outsource at least some of their operations, according to the U.S. Small Business Administration. Bookkeeping sits at the top of that list.

But here's the thing: handing off financial data to a third party isn't a casual decision. There are cost structures to decode, compliance rules to respect, and provider quality to vet.

This guide walks through everything—what bookkeeping outsourcing actually means, when it makes sense, what it costs, and how to choose a provider that won't create more headaches than it solves.

What Is Bookkeeping Outsourcing?

Bookkeeping outsourcing means hiring an external individual or firm to handle the day-to-day financial record-keeping tasks that keep a business compliant and financially transparent.

These tasks include transaction recording, bank reconciliation, accounts payable and receivable management, payroll processing, expense categorization, and monthly financial statement preparation.

The external provider operates remotely, accessing accounting software and financial systems through secure cloud platforms. Some businesses outsource selectively—handing off just payroll or invoice processing. Others delegate the entire bookkeeping function.

How It Differs From In-House Bookkeeping

An in-house bookkeeper is a direct employee. Salary, benefits, office space, software licenses, training, and management overhead all fall on the business.

An outsourced bookkeeper works as a contractor or through a firm. The business pays a fixed monthly fee or hourly rate. No benefits, no desk, no HR paperwork.

And if transaction volume doubles during a growth phase? The outsourced provider scales capacity. No need to hire, onboard, or train additional staff.

When Should Businesses Outsource Bookkeeping?

Timing matters. Outsource too early, and you're paying for services you could handle with a spreadsheet. Wait too long, and you're buried in compliance errors and cash flow blind spots.

Signs It's Time to Outsource

Transaction volume becomes unmanageable. Once monthly transactions exceed a few dozen, manual tracking breaks down. Errors creep in, reconciliation takes hours, and reporting lags behind decision-making needs.

Tax filing stress intensifies. If quarterly tax prep feels like archaeology—digging through receipts, reconstructing expenses, guessing at deductions—the books aren't being kept properly.

Growth outpaces administrative capacity. Scaling a business demands focus on revenue-generating activities. When bookkeeping consumes ten hours a week, that's ten hours not spent on product development, sales, or strategy.

Compliance requirements tighten. Regulated industries, grant-funded organizations, and venture-backed startups face stricter reporting standards. Mistakes carry financial and legal consequences.

Hiring a full-time bookkeeper doesn't pencil out. A mid-level bookkeeper costs north of $60,000 annually, plus benefits and overhead. For many businesses, that's budget they don't have—or would rather allocate elsewhere.

Build Bookkeeping Support with NeoWork

Bookkeeping outsourcing helps businesses stay on top of financial records, document updates, and recurring accounting support tasks. NeoWork provides remote teammates who can help with bookkeeping support, data entry, records organization, and administrative finance workflows. NeoWork handles recruitment, benefits, training, and ongoing engagement, while teammates work inside the client’s tools and day-to-day processes. Its 91% annualized teammate retention rate and 3.2% candidate selectivity rate reflect a focus on selective hiring and longer-term team stability.

NeoWork's bookkeeping support model offers:

- bookkeeping and financial data support

- integration with the client’s tools and processes

- recruitment and ongoing teammate support

Contact NeoWork to build bookkeeping support that keeps daily finance work moving.

The Cost Structure of Bookkeeping Outsourcing

Pricing varies widely based on transaction volume, complexity, industry, and service scope. Here's what the market looks like.

Freelance Bookkeepers

Freelance bookkeepers typically charge $200–$500 per month for basic services—transaction recording, bank reconciliation, and simple financial statements.

Hourly rates range from $20 to $150, depending on expertise and task complexity. Routine data entry sits at the lower end. Tax-adjacent work, multi-entity consolidation, and industry-specific reporting command higher rates.

Bookkeeping Firms

Established bookkeeping firms charge $500–$2,500 per month. The fee scales with transaction volume, number of accounts, payroll complexity, and reporting requirements.

Firms offer more stability than freelancers. They have backup staff, standardized processes, and often provide integrated services like controller-level oversight or CFO advisory.

Virtual CFO and Controller Services

At the top end, virtual CFO services start around $2,500 per month. These providers go beyond bookkeeping—they deliver financial analysis, budgeting, forecasting, and strategic guidance.

For businesses preparing to scale, raise capital, or navigate complex financial decisions, this tier makes sense. For straightforward record-keeping, it's overkill.

Factors That Influence Pricing

Several variables push costs up or down.

Benefits of Outsourcing Bookkeeping

The advantages go beyond just cost savings—though that's a big one.

Reduced Overhead

Some sources indicate potential savings through outsourcing bookkeeping services compared to in-house operations. No salary, no payroll taxes, no benefits, no office space, no software licenses beyond what's already in use.

That total package for an in-house mid-level professional can easily exceed $60,000 annually. A fixed monthly fee for external service delivers the same output for a fraction of the overhead.

Access to Specialized Expertise

Outsourced bookkeepers work with multiple clients across industries. They've seen edge cases, handled complex reconciliations, and navigated software quirks that would stump a generalist.

Need someone who understands construction job costing? Or nonprofit fund accounting? Or multi-currency e-commerce? Specialized providers exist.

Scalability and Flexibility

Hiring a full-time employee locks in fixed capacity. If the business grows, you need another hire. If it contracts, you're overstaffed.

Outsourced providers scale service levels up or down based on need. Seasonal businesses, high-growth startups, and companies with fluctuating transaction volumes benefit most.

Focus on Core Business Activities

Bookkeeping doesn't generate revenue. It supports operations, but it's not product development, sales, or customer service.

Delegating financial record-keeping frees up time and mental bandwidth for activities that directly drive growth.

Improved Accuracy and Compliance

Professional bookkeepers stay current on tax regulations, reporting standards, and compliance requirements. They catch errors before they cascade into tax penalties or audit issues.

For businesses subject to oversight—whether from investors, lenders, or regulatory bodies—clean, accurate books aren't optional.

Drawbacks and Risks of Outsourcing

Outsourcing isn't a silver bullet. It introduces trade-offs and risks that need managing.

Loss of Direct Control

When bookkeeping happens in-house, the business owner has direct oversight. Questions get answered immediately. Adjustments happen in real time.

Outsourcing introduces a layer of separation. Communication happens via email or video calls. Turnaround times vary.

Data Security Concerns

Financial data is sensitive. Bank account details, payroll information, vendor contracts—all of it flows through the bookkeeper's systems.

Third-party access creates risk. If the provider's security protocols are weak, or if they suffer a breach, the business's financial data is exposed.

Communication and Time Zone Challenges

Many outsourced bookkeepers operate remotely, sometimes internationally. Time zone differences can delay responses. Cultural or language barriers may complicate nuanced financial discussions.

Potential for Service Inconsistency

Freelancers get sick, take vacations, or move on to other clients. If there's no backup, work stalls.

Firms offer more continuity, but staff turnover still happens. A new bookkeeper assigned to the account needs time to ramp up.

Compliance and Regulatory Considerations

Outsourcing doesn't absolve the business of compliance responsibility. Tax authorities hold the business accountable—not the bookkeeper.

IRS Rules on Tax Return Preparer Disclosure

The IRS Section 7216 regulations govern the disclosure and use of tax return information by preparers. Final Treasury Regulations on consent requirements became effective December 28, 2012.

These rules require explicit consent before a tax preparer can use or disclose client tax information. Businesses outsourcing bookkeeping to firms that also prepare tax returns must ensure proper consent forms are in place.

Circular 230 and Professional Standards

The Office of Professional Responsibility (OPR) enforces Treasury Department Circular 230, which establishes standards of competence, integrity, and conduct for tax professionals.

Enrolled agents, CPAs, and attorneys who represent taxpayers before the IRS must adhere to these standards and complete 72 hours of continuing education every three years. When vetting providers, confirming credentials matters.

SOC 2 Compliance for Service Organizations

The American Institute of CPAs (AICPA) offers System and Organization Controls (SOC) reporting for service organizations. SOC 2 reports assess controls relevant to security, availability, processing integrity, confidentiality, and privacy.

For businesses outsourcing financial functions, working with a SOC 2–compliant provider offers third-party validation that the vendor's controls are sound. This is especially important for regulated industries or businesses handling sensitive customer data.

How to Choose the Right Bookkeeping Provider

Vetting providers takes effort. But picking the wrong one creates problems that cost far more than the monthly fee.

Assess Your Needs First

Before contacting providers, map out what needs to be done. Transaction volume, number of accounts, payroll complexity, reporting frequency, industry-specific requirements—all of this shapes the scope.

A clear scope makes it easier to compare proposals and spot providers who don't understand the ask.

Verify Credentials and Experience

Ask about certifications. Are the bookkeepers CPAs, enrolled agents, or certified bookkeepers? Do they carry professional liability insurance?

Request client references, especially from businesses in the same industry. A provider experienced with e-commerce may struggle with nonprofit fund accounting.

Evaluate Technology and Integration

Most businesses already use accounting software—QuickBooks, Xero, FreshBooks, NetSuite. The provider needs to work fluently within that system.

Ask about integration capabilities, data security protocols, and backup procedures. How is data transmitted? Where is it stored? Who has access?

Understand Communication and Reporting

How often will reports be delivered? What format? How quickly do they respond to questions?

Clarify who the primary point of contact will be and whether there's backup coverage if that person is unavailable.

Review Service Agreements Carefully

Service agreements should spell out scope, deliverables, turnaround times, pricing, termination terms, and data ownership.

Pay attention to clauses around confidentiality, data breach notification, and liability limitations.

Common Bookkeeping Tasks to Outsource

Not every business outsources the entire bookkeeping function. Many start with specific tasks.

Transaction Recording and Categorization

Every sale, purchase, payment, and receipt needs to be logged and categorized. This is the foundation of bookkeeping and the most time-consuming piece.

Bank and Credit Card Reconciliation

Monthly reconciliation ensures the accounting records match bank statements. Discrepancies signal errors, fraud, or missing transactions.

Accounts Payable and Receivable Management

Tracking what the business owes and what customers owe keeps cash flow visible. Late vendor payments damage relationships. Overdue customer invoices hurt liquidity.

Payroll Processing

Payroll is high-stakes. Errors trigger employee dissatisfaction, tax penalties, and compliance headaches. Outsourcing payroll reduces risk and administrative burden.

Financial Statement Preparation

Monthly profit and loss statements, balance sheets, and cash flow reports provide the financial snapshot needed for decision-making. Clean, timely financials are non-negotiable for businesses seeking funding or managing growth.

Outsourcing vs. In-House: A Direct Comparison

The choice isn't always binary, but understanding the trade-offs helps.

Mistakes to Avoid When Outsourcing Bookkeeping

Several pitfalls trip up businesses new to outsourcing.

Choosing Based on Price Alone

The cheapest provider isn't always the best value. Low rates often correlate with inexperience, high error rates, or poor communication.

Focus on qualifications, references, and service quality—not just the monthly fee.

Failing to Define Scope Clearly

Ambiguous agreements lead to mismatched expectations. The business assumes certain tasks are included. The provider disagrees. Frustration and extra charges follow.

Document everything: what tasks are covered, what deliverables are expected, and what timelines apply.

Neglecting Data Security

Not all providers implement robust security measures. Weak encryption, shared logins, or unsecured file transfers expose sensitive financial data.

Ask specific questions about security protocols, compliance certifications, and breach response plans.

Ignoring Red Flags During Vetting

Delayed responses during the sales process, vague answers about credentials, reluctance to provide references—these are warning signs.

If something feels off during the vetting phase, it won't improve after the contract is signed.

The Future of Bookkeeping Outsourcing

Automation, artificial intelligence, and cloud-based collaboration are reshaping how bookkeeping services are delivered.

AI-powered tools now categorize transactions, flag anomalies, and generate reports with minimal human intervention. This reduces the manual workload and lowers costs—but it also raises the bar for human bookkeepers to deliver strategic value beyond data entry.

Cloud accounting platforms enable real-time collaboration between businesses and their outsourced providers. Gone are the days of mailing spreadsheets or scheduling file transfers. Both parties access the same live data, speeding up reconciliation and reporting.

For businesses, this means faster close cycles, better visibility, and more responsive financial management. For providers, it means higher efficiency and the ability to serve more clients without sacrificing quality.

Conclusion

Bookkeeping outsourcing offers a practical path for businesses looking to reduce overhead, access specialized expertise, and scale financial operations without the commitment of full-time hires.

But it's not a hands-off solution. Compliance responsibility remains with the business. Data security demands vigilance. Provider selection requires thorough vetting.

When done right—clear scope, credentialed provider, strong controls—outsourcing transforms bookkeeping from a time-draining burden into a streamlined, scalable function that supports growth.

Ready to explore outsourcing? Start by mapping your needs, setting a realistic budget, and interviewing providers who specialize in your industry. The right partnership pays dividends in accuracy, time savings, and financial clarity.

Frequently Asked Questions

Topics

Related Blogs

Related Podcasts