.avif)

.avif)

Insurance Claims Management Outsourcing Guide 2026

Quick Summary: Insurance claims management outsourcing transfers claims handling, processing, and adjudication to specialized third-party providers, reducing operational costs by 10-35% while improving turnaround times and accuracy. This guide covers the benefits, implementation strategy, vendor selection, and best practices to help insurers optimize claims operations.

What Is Insurance Claims Management Outsourcing?

Insurance claims management outsourcing is the delegation of claims-related operations to external service providers who specialize in handling the entire lifecycle of a claim—from initial intake through final settlement. Rather than maintaining an in-house claims team, insurers partner with Business Process Outsourcing (BPO) firms to manage document verification, data entry, fraud detection, adjudication, and customer communication.

The service model is flexible. Some insurers outsource specific tasks like document processing, while others transfer the entire claims operation. This approach has become increasingly common as insurers seek operational efficiency without sacrificing quality or compliance.

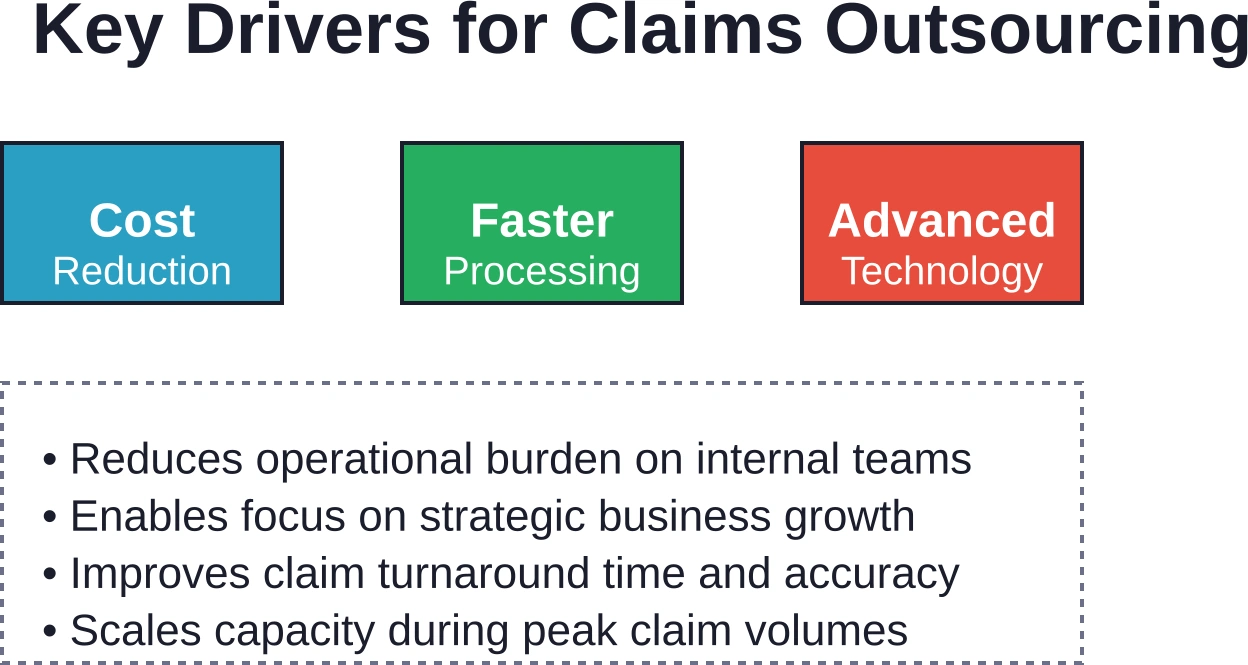

Why Insurers Are Turning to Claims Outsourcing

Claims processing represents one of the most resource-intensive functions in insurance. According to Deloitte-led projects, outsourcing has delivered cost reductions ranging from 10% to 35% for pan-European companies. Beyond cost, there's the matter of speed and accuracy—two factors that directly impact customer retention and regulatory standing.

Filing an insurance claim is often the moment of truth for policyholders. If the process drags on or errors occur, customers leave. Outsourcing to specialized providers with proven track records, advanced technology, and scalable infrastructure helps insurers deliver on their promise when it matters most.

Measurable Benefits of Claims Management Outsourcing

The case for outsourcing rests on concrete operational and financial gains. According to Deloitte research, pan-European companies using outsourcing partners achieved internal operational cost reductions between 10% to 35%. These aren't theoretical numbers—they reflect actual project outcomes.

Beyond cost, outsourcing delivers measurable improvements in processing speed. Automated document classification achieves accuracy rates up to 98%, and labor-intensive data entry workloads drop by 70%. For insurers, this means faster claim resolution and reduced manual errors that trigger rework and customer complaints.

Scalability Without Fixed Overhead

Third-party providers can adjust capacity based on seasonal claim volumes. During peak periods—natural disasters, flu season, or major accidents—outsourcing partners scale up resources without the insurer incurring permanent payroll commitments. This flexibility keeps costs aligned with demand.

Access to Specialized Expertise

Top claims outsourcing firms employ specialists trained in fraud detection, regulatory compliance, and complex claim adjudication. They invest in technology that individual insurers might not justify building in-house. This expertise translates to better decision-making and reduced fraud losses.

How to Select the Right Claims Outsourcing Partner

Choosing a vendor is the most critical decision in the outsourcing process. A poor fit creates problems that no amount of cost savings can offset.

Step 1: Assess Your Current State

Before reaching out to vendors, conduct an internal audit. How many claims does your team process monthly? What's the average turnaround time? Which processes consume the most labor? What compliance frameworks apply? This baseline helps you define requirements and measure improvement later.

Step 2: Build a Clear RFP (Request for Proposal)

Document exactly what you need outsourced—specific processes, volume, turnaround targets, compliance requirements, and technology needs. A thorough RFP narrows the field and prevents misaligned expectations later. Include questions about their technology stack, security practices, industry experience, and references.

Step 3: Evaluate Shortlisted Vendors

Look beyond pricing. Assess their technology capabilities, team experience, security certifications, regulatory knowledge, and track record with similar-sized clients. Request demos of their platform, sample workflows, and detailed case studies. Talk to their existing clients about responsiveness, quality, and problem-solving.

Step 4: Pilot Before Full Commitment

Many successful outsourcing partnerships start with a pilot phase—handling a subset of claims or a specific process segment for 3-6 months. This lets both sides test the fit, identify gaps, and adjust before committing to full-scale operations. It's far cheaper to discover issues during a pilot than to renegotiate mid-contract.

Keep Insurance Claims Work Moving with NeoWork

Insurance claims management can create pressure when teams have to manage patient billing, reimbursements, insurance communication, documentation, and follow-ups at the same time. NeoWork supports healthcare organizations with dedicated medical claims administrators and specialists who can help with claims-related administrative work.

For healthcare providers and healthcare companies, this can include medical claims administration, patient billing support, insurance coordination, reimbursements, denial-related follow-up, documentation, and patient account communication. NeoWork reports a 91% annualized teammate retention rate and a 3.2% candidate selectivity rate, which matters when claims work depends on accuracy, process familiarity, and steady execution.

Insurance claims tasks NeoWork can support:

- medical claims administration

- patient billing and reimbursement support

- insurance coordination and follow-ups

- documentation and patient account communication

Contact NeoWork to build insurance claims support that keeps revenue cycle tasks organized, reduces administrative bottlenecks, and gives your internal team more room to focus on higher-priority work.

Common Risks and Mitigation Strategies

Outsourcing isn't without risks. Data security and regulatory compliance top the list of concerns, followed by potential quality gaps and loss of process control. The key is selecting the right partner and maintaining oversight.

Implementation Best Practices

A successful rollout requires planning and change management. Following Deloitte's strategic outsourcing framework, there are five critical phases.

Phase 1: Rightsizing the Deal

Define the exact scope. Which processes go to the vendor? Which stay in-house? What's the service level agreement (SLA)—turnaround times, accuracy targets, availability? Be specific. Vague scope leads to disputes and cost overruns.

Phase 2: Building a Solid Foundation

Prepare your organization and processes. Clean up data, document workflows, and identify any legacy systems that need replacement. Brief your internal team on the transition. Establish the governance structure—who approves changes, who escalates issues, who reviews performance?

Phase 3: Vendor Selection

Run a competitive RFP process. Evaluate at least three qualified vendors. Don't focus solely on price; factor in technology, expertise, and cultural alignment. The cheapest option often isn't the best value.

Phase 4: Striking the Deal

Negotiate terms carefully. Protect yourself with clear penalties for missing SLAs, data breach clauses, and termination rights. Ensure the contract specifies what happens if the vendor underperforms or goes out of business.

Phase 5: After the Deal Is Signed

This is where many partnerships fail. Establish a governance cadence—weekly operational reviews, monthly performance reviews, quarterly strategy sessions. Monitor KPIs against targets. Address issues promptly. Invest in the relationship.

Technology and Automation in Claims Outsourcing

Modern claims outsourcing partners deploy AI and machine learning to augment human judgment. Automated workflows extract data from documents, classify claim types, flag potential fraud, and route cases to the right adjudicator. These tools don't replace people—they amplify their capacity and accuracy.

Gartner reports that BPO models can deliver up to 30% operational cost reduction, much of which stems from intelligent automation. When paired with human expertise, this combination yields both speed and quality.

Looking Ahead: Future Trends in Claims Outsourcing

The industry is moving toward deeper automation and AI integration. Deloitte research shows that while 57% of organizations are using agentic AI (autonomous AI systems), only 10% have realized significant ROI to date. However, 50% expect ROI within three years, and 33% anticipate it within three to five years.

For claims outsourcing, this means partners will increasingly automate not just data entry but actual claim adjudication decisions. Fraud detection will become more sophisticated. Real-time dashboards will give insurers unprecedented visibility. The best firms are already positioning for this shift, investing in AI expertise and building platforms designed for autonomous workflows.

Final Takeaway

Insurance claims management outsourcing is no longer a novelty—it's a proven strategy deployed by leading insurers worldwide. The financial case is clear: cost reductions of 10-35%, faster turnaround, and improved accuracy. The operational case is equally strong: scalable capacity, access to expertise, and the ability to focus internal talent on strategic initiatives.

Success depends on three things: selecting the right partner, setting clear expectations, and maintaining active governance throughout the relationship. Don't outsource to a vendor you wouldn't trust with your customer relationships. Take time with vendor selection. Run a pilot. Monitor performance relentlessly. When these fundamentals are in place, claims outsourcing delivers substantial value.

Ready to explore claims outsourcing for your organization? Start by auditing your current state, defining your requirements, and identifying potential vendors. A structured approach to vendor selection and implementation will position you for success.

Frequently Asked Questions

Topics

Insurance Claims Management Outsourcing Guide 2026

Quick Summary: Insurance claims management outsourcing transfers claims handling, processing, and adjudication to specialized third-party providers, reducing operational costs by 10-35% while improving turnaround times and accuracy. This guide covers the benefits, implementation strategy, vendor selection, and best practices to help insurers optimize claims operations.

What Is Insurance Claims Management Outsourcing?

Insurance claims management outsourcing is the delegation of claims-related operations to external service providers who specialize in handling the entire lifecycle of a claim—from initial intake through final settlement. Rather than maintaining an in-house claims team, insurers partner with Business Process Outsourcing (BPO) firms to manage document verification, data entry, fraud detection, adjudication, and customer communication.

The service model is flexible. Some insurers outsource specific tasks like document processing, while others transfer the entire claims operation. This approach has become increasingly common as insurers seek operational efficiency without sacrificing quality or compliance.

Why Insurers Are Turning to Claims Outsourcing

Claims processing represents one of the most resource-intensive functions in insurance. According to Deloitte-led projects, outsourcing has delivered cost reductions ranging from 10% to 35% for pan-European companies. Beyond cost, there's the matter of speed and accuracy—two factors that directly impact customer retention and regulatory standing.

Filing an insurance claim is often the moment of truth for policyholders. If the process drags on or errors occur, customers leave. Outsourcing to specialized providers with proven track records, advanced technology, and scalable infrastructure helps insurers deliver on their promise when it matters most.

Measurable Benefits of Claims Management Outsourcing

The case for outsourcing rests on concrete operational and financial gains. According to Deloitte research, pan-European companies using outsourcing partners achieved internal operational cost reductions between 10% to 35%. These aren't theoretical numbers—they reflect actual project outcomes.

Beyond cost, outsourcing delivers measurable improvements in processing speed. Automated document classification achieves accuracy rates up to 98%, and labor-intensive data entry workloads drop by 70%. For insurers, this means faster claim resolution and reduced manual errors that trigger rework and customer complaints.

Scalability Without Fixed Overhead

Third-party providers can adjust capacity based on seasonal claim volumes. During peak periods—natural disasters, flu season, or major accidents—outsourcing partners scale up resources without the insurer incurring permanent payroll commitments. This flexibility keeps costs aligned with demand.

Access to Specialized Expertise

Top claims outsourcing firms employ specialists trained in fraud detection, regulatory compliance, and complex claim adjudication. They invest in technology that individual insurers might not justify building in-house. This expertise translates to better decision-making and reduced fraud losses.

How to Select the Right Claims Outsourcing Partner

Choosing a vendor is the most critical decision in the outsourcing process. A poor fit creates problems that no amount of cost savings can offset.

Step 1: Assess Your Current State

Before reaching out to vendors, conduct an internal audit. How many claims does your team process monthly? What's the average turnaround time? Which processes consume the most labor? What compliance frameworks apply? This baseline helps you define requirements and measure improvement later.

Step 2: Build a Clear RFP (Request for Proposal)

Document exactly what you need outsourced—specific processes, volume, turnaround targets, compliance requirements, and technology needs. A thorough RFP narrows the field and prevents misaligned expectations later. Include questions about their technology stack, security practices, industry experience, and references.

Step 3: Evaluate Shortlisted Vendors

Look beyond pricing. Assess their technology capabilities, team experience, security certifications, regulatory knowledge, and track record with similar-sized clients. Request demos of their platform, sample workflows, and detailed case studies. Talk to their existing clients about responsiveness, quality, and problem-solving.

Step 4: Pilot Before Full Commitment

Many successful outsourcing partnerships start with a pilot phase—handling a subset of claims or a specific process segment for 3-6 months. This lets both sides test the fit, identify gaps, and adjust before committing to full-scale operations. It's far cheaper to discover issues during a pilot than to renegotiate mid-contract.

Keep Insurance Claims Work Moving with NeoWork

Insurance claims management can create pressure when teams have to manage patient billing, reimbursements, insurance communication, documentation, and follow-ups at the same time. NeoWork supports healthcare organizations with dedicated medical claims administrators and specialists who can help with claims-related administrative work.

For healthcare providers and healthcare companies, this can include medical claims administration, patient billing support, insurance coordination, reimbursements, denial-related follow-up, documentation, and patient account communication. NeoWork reports a 91% annualized teammate retention rate and a 3.2% candidate selectivity rate, which matters when claims work depends on accuracy, process familiarity, and steady execution.

Insurance claims tasks NeoWork can support:

- medical claims administration

- patient billing and reimbursement support

- insurance coordination and follow-ups

- documentation and patient account communication

Contact NeoWork to build insurance claims support that keeps revenue cycle tasks organized, reduces administrative bottlenecks, and gives your internal team more room to focus on higher-priority work.

Common Risks and Mitigation Strategies

Outsourcing isn't without risks. Data security and regulatory compliance top the list of concerns, followed by potential quality gaps and loss of process control. The key is selecting the right partner and maintaining oversight.

Implementation Best Practices

A successful rollout requires planning and change management. Following Deloitte's strategic outsourcing framework, there are five critical phases.

Phase 1: Rightsizing the Deal

Define the exact scope. Which processes go to the vendor? Which stay in-house? What's the service level agreement (SLA)—turnaround times, accuracy targets, availability? Be specific. Vague scope leads to disputes and cost overruns.

Phase 2: Building a Solid Foundation

Prepare your organization and processes. Clean up data, document workflows, and identify any legacy systems that need replacement. Brief your internal team on the transition. Establish the governance structure—who approves changes, who escalates issues, who reviews performance?

Phase 3: Vendor Selection

Run a competitive RFP process. Evaluate at least three qualified vendors. Don't focus solely on price; factor in technology, expertise, and cultural alignment. The cheapest option often isn't the best value.

Phase 4: Striking the Deal

Negotiate terms carefully. Protect yourself with clear penalties for missing SLAs, data breach clauses, and termination rights. Ensure the contract specifies what happens if the vendor underperforms or goes out of business.

Phase 5: After the Deal Is Signed

This is where many partnerships fail. Establish a governance cadence—weekly operational reviews, monthly performance reviews, quarterly strategy sessions. Monitor KPIs against targets. Address issues promptly. Invest in the relationship.

Technology and Automation in Claims Outsourcing

Modern claims outsourcing partners deploy AI and machine learning to augment human judgment. Automated workflows extract data from documents, classify claim types, flag potential fraud, and route cases to the right adjudicator. These tools don't replace people—they amplify their capacity and accuracy.

Gartner reports that BPO models can deliver up to 30% operational cost reduction, much of which stems from intelligent automation. When paired with human expertise, this combination yields both speed and quality.

Looking Ahead: Future Trends in Claims Outsourcing

The industry is moving toward deeper automation and AI integration. Deloitte research shows that while 57% of organizations are using agentic AI (autonomous AI systems), only 10% have realized significant ROI to date. However, 50% expect ROI within three years, and 33% anticipate it within three to five years.

For claims outsourcing, this means partners will increasingly automate not just data entry but actual claim adjudication decisions. Fraud detection will become more sophisticated. Real-time dashboards will give insurers unprecedented visibility. The best firms are already positioning for this shift, investing in AI expertise and building platforms designed for autonomous workflows.

Final Takeaway

Insurance claims management outsourcing is no longer a novelty—it's a proven strategy deployed by leading insurers worldwide. The financial case is clear: cost reductions of 10-35%, faster turnaround, and improved accuracy. The operational case is equally strong: scalable capacity, access to expertise, and the ability to focus internal talent on strategic initiatives.

Success depends on three things: selecting the right partner, setting clear expectations, and maintaining active governance throughout the relationship. Don't outsource to a vendor you wouldn't trust with your customer relationships. Take time with vendor selection. Run a pilot. Monitor performance relentlessly. When these fundamentals are in place, claims outsourcing delivers substantial value.

Ready to explore claims outsourcing for your organization? Start by auditing your current state, defining your requirements, and identifying potential vendors. A structured approach to vendor selection and implementation will position you for success.

Frequently Asked Questions

Topics

Related Blogs

Related Podcasts