.avif)

.avif)

Insurance Policy Administration Outsourcing Guide 2026

Quick Summary: Insurance policy administration outsourcing helps carriers, MGAs, and agencies streamline operations by delegating labor-intensive tasks to specialized service providers. This guide covers the key benefits, process steps, challenges, and best practices for choosing the right outsourcing partner.

What Is Insurance Policy Administration?

Insurance policy administration encompasses the day-to-day operational tasks required to manage policies throughout their lifecycle. This includes policy creation, data entry, documentation, premium accounting, customer service, and policy updates.

The process begins when a customer applies for coverage. Information flows through underwriting, approval, issuance, and servicing phases. Every step requires accurate data handling, compliance with regulatory standards, and timely communication with policyholders.

For small agencies, this work is manageable. But as policy volumes grow—especially for carriers, managing general agents (MGAs), and wholesalers—the administrative burden becomes substantial. Manual processes slow turnaround times, increase error rates, and tie up staff who could focus on sales and strategy.

Why Insurance Policy Administration Is Critical

Effective administration directly impacts customer satisfaction, regulatory compliance, and profitability. Policies that aren't processed accurately create downstream problems: premium billing errors, coverage gaps, compliance violations, and customer dissatisfaction.

Real talk: a single administrative glitch can be costly. Consider the BNY Mellon case—a Massachusetts regulator fined the firm $3 million in March 2016 over an administrative error in policy handling. Mistakes compound quickly in insurance operations.

Sound familiar? Insurance companies increasingly rely on policy administration systems to reduce manual work. But systems alone aren't enough without skilled staff to operate them consistently.

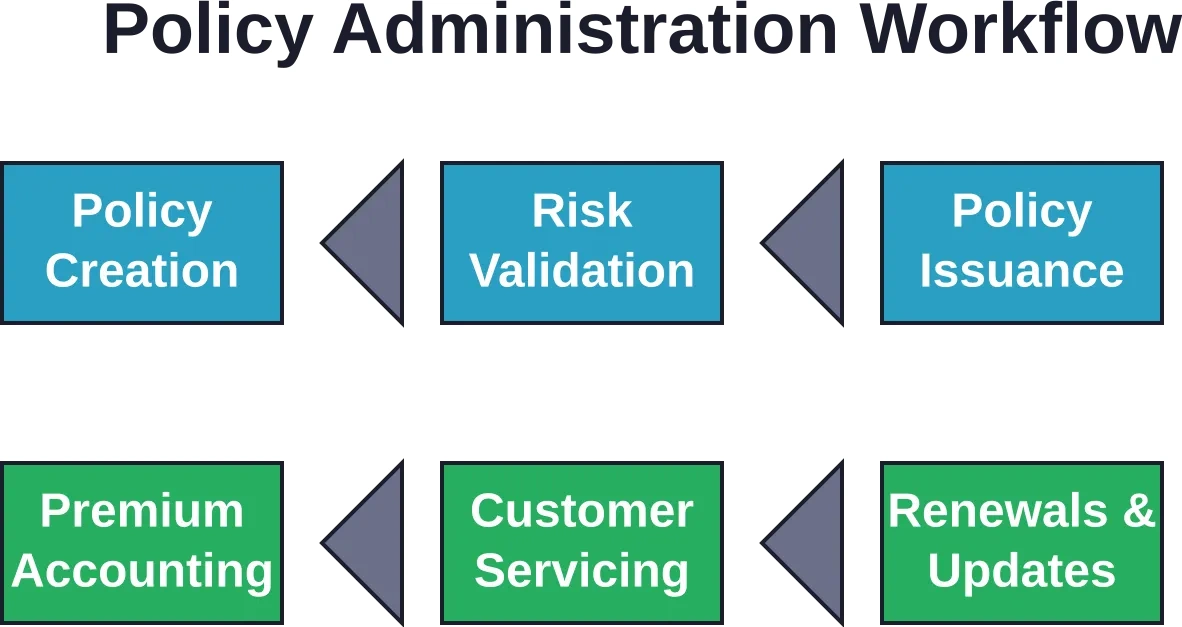

Step-by-Step Insurance Policy Administration Process

Understanding the core workflow helps explain why outsourcing has become attractive. Here's how the process flows:

Policy Creation

Initial policyholder information and coverage details are captured and entered into the system. Accuracy here matters—mistakes propagate through the entire lifecycle.

Risk Validation

Underwriting teams review policy details to ensure they meet company standards and regulatory requirements. This phase determines whether the policy can proceed.

Policy Issuance

Once approved, the policy is formally issued. Documentation is prepared, contracts are generated, and the policyholder receives their coverage details.

Premium Accounting & Customer Servicing

Ongoing tasks include processing payments, handling claims, managing policy changes, and responding to customer inquiries. These tasks repeat continuously throughout the policy term.

Renewals and Updates

As policies approach renewal, servicing teams initiate renewal processes. Policyholders may request coverage updates, address changes, or coverage adjustments—each requiring documentation and system updates.

Key Challenges in Policy Administration

Why do insurance companies struggle with policy administration? The answer lies in volume, complexity, and resource constraints.

Why Outsource Insurance Policy Administration?

Insurance policy processing is one of the most operationally intensive tasks within insurance organizations. Outsourcing transfers these labor-intensive functions to dedicated service providers who specialize in managing them.

Cost Efficiency

Outsourcing reduces payroll overhead, eliminates the cost of recruiting and training staff, and avoids the expense of maintaining infrastructure. Providers achieve economies of scale by handling policies for multiple clients.

Operational Efficiency

Outsourcing partners use standardized processes and technology platforms optimized for policy administration. Tasks are completed faster with fewer errors. Organizations like Strada report answering 85%+ of calls and providing 24/7/365 availability, ensuring workflows keep moving smoothly.

Focus on Core Business

Internal teams can redirect their attention to sales, underwriting, customer relationships, and strategic growth instead of routine administrative work. This shift improves overall business performance.

Scalability

As policy volumes fluctuate, outsourcing partners scale resources up or down. Companies avoid the fixed cost of maintaining a large internal team during slow periods.

Compliance and Risk Management

According to the Department of Labor, outsourcing employee benefit plan services allows plan sponsors to gain access to expertise and technology while maintaining oversight. Outsourcing partners stay current with regulatory changes and implement controls to minimize compliance risk.

Types of Tasks to Outsource

Not all policy administration functions need outsourcing. Here's what typically makes sense to delegate:

- Data Entry and Processing: Converting application forms into system records

- Documentation: Preparing policies, contracts, and correspondence

- Premium Accounting: Processing payments, managing billing cycles, reconciling accounts

- Customer Support: Answering routine inquiries, processing address changes, handling service requests

- Claims Support: Managing claim documentation and initial claim processing

- Renewals Administration: Generating renewal notices, processing renewal applications

Functions that typically remain internal include underwriting decisions, claims approval authority, and strategic policy management.

Choosing the Right Outsourcing Partner

Not all outsourcing providers are equal. Here's what to do:

- Take time to ask detailed questions.

- Request references from current clients in your segment.

- Understand their technology stack and how it integrates with yours.

- Verify certifications and compliance credentials.

Add Policy Administration Support with NeoWork

Insurance policy administration outsourcing can help insurers manage routine customer and back-office work without overloading internal teams. NeoWork supports insurance operations through staffing and operational support, including customer experience management, administrative support, claims processing, compliance support, and policy support. Their 91% annualized teammate retention rate and 3.2% candidate selectivity rate are especially useful for policy administration because support teams need to understand internal processes, customer expectations, and recurring documentation requirements.

Policy administration tasks NeoWork can provide:

- policy information and documentation support

- billing-related admin and follow-ups

- claims, compliance, and back-office support

👉Contact NeoWork to add policy administration support that keeps routine insurance workflows organized, improves customer response consistency, and reduces pressure on internal teams.

Outsourcing Models: Onshore vs. Offshore

Two primary outsourcing approaches exist, each with trade-offs:

Many insurers use hybrid models—combining onshore account management with offshore processing to balance costs and control.

Best Practices for Successful Outsourcing

Successful outsourcing requires more than just selecting a vendor. Here's what works:

Clear Scope Definition

Define exactly what work is being outsourced, including volume expectations, quality standards, and timelines. Ambiguity leads to disputes and poor outcomes.

Strong Service Level Agreements

Establish measurable SLAs covering turnaround times, accuracy rates, availability, and escalation procedures. These protect your business and provide accountability.

Ongoing Monitoring

Don't hand off work and disappear. Monitor quality, volume, compliance, and cost metrics regularly. Schedule reviews with the partner to discuss performance and improvement opportunities.

Secure Knowledge Transfer

Invest time in training the outsourcing team on your policies, procedures, systems, and business requirements. Poor knowledge transfer is a leading cause of outsourcing failure.

Maintain Internal Oversight

As noted by the SEC's guidance on outsourcing by investment advisers, organizations cannot waive their fiduciary duty. The organization must oversee outsourced functions to ensure legal obligations are met, regardless of who performs the work.

Common Outsourcing Pitfalls

But wait—outsourcing isn't without risk. Watch out for these common mistakes:

- Choosing Solely on Price: The cheapest option often delivers the poorest quality, creating expensive problems later

- Inadequate Due Diligence: Failing to verify provider credentials, capabilities, and stability exposes your business to operational risk

- Poor Communication: Unclear expectations and infrequent check-ins lead to misalignment and mistakes

- Losing Control: Over-delegating without maintaining oversight violates fiduciary responsibilities and creates compliance exposure

- Rapid Scaling: Growing volumes too quickly without adequate quality controls overwhelms the partner and degrades service

Conclusion

Insurance policy administration outsourcing isn't a one-size-fits-all solution. But for carriers, MGAs, wholesalers, and agencies drowning in administrative work, it's a practical way to reduce costs, improve efficiency, and refocus energy on business growth.

Success requires careful partner selection, clear contractual terms, ongoing monitoring, and maintained internal oversight. The investment in proper outsourcing governance pays dividends through improved operations and reduced compliance risk.

Ready to evaluate outsourcing for your organization? Start by documenting your current processes, estimating volumes and costs, and identifying which tasks are candidates for delegation. Then request proposals from qualified providers and compare their capabilities, pricing, and fit for your business.

Frequently Asked Questions

Topics

Insurance Policy Administration Outsourcing Guide 2026

Quick Summary: Insurance policy administration outsourcing helps carriers, MGAs, and agencies streamline operations by delegating labor-intensive tasks to specialized service providers. This guide covers the key benefits, process steps, challenges, and best practices for choosing the right outsourcing partner.

What Is Insurance Policy Administration?

Insurance policy administration encompasses the day-to-day operational tasks required to manage policies throughout their lifecycle. This includes policy creation, data entry, documentation, premium accounting, customer service, and policy updates.

The process begins when a customer applies for coverage. Information flows through underwriting, approval, issuance, and servicing phases. Every step requires accurate data handling, compliance with regulatory standards, and timely communication with policyholders.

For small agencies, this work is manageable. But as policy volumes grow—especially for carriers, managing general agents (MGAs), and wholesalers—the administrative burden becomes substantial. Manual processes slow turnaround times, increase error rates, and tie up staff who could focus on sales and strategy.

Why Insurance Policy Administration Is Critical

Effective administration directly impacts customer satisfaction, regulatory compliance, and profitability. Policies that aren't processed accurately create downstream problems: premium billing errors, coverage gaps, compliance violations, and customer dissatisfaction.

Real talk: a single administrative glitch can be costly. Consider the BNY Mellon case—a Massachusetts regulator fined the firm $3 million in March 2016 over an administrative error in policy handling. Mistakes compound quickly in insurance operations.

Sound familiar? Insurance companies increasingly rely on policy administration systems to reduce manual work. But systems alone aren't enough without skilled staff to operate them consistently.

Step-by-Step Insurance Policy Administration Process

Understanding the core workflow helps explain why outsourcing has become attractive. Here's how the process flows:

Policy Creation

Initial policyholder information and coverage details are captured and entered into the system. Accuracy here matters—mistakes propagate through the entire lifecycle.

Risk Validation

Underwriting teams review policy details to ensure they meet company standards and regulatory requirements. This phase determines whether the policy can proceed.

Policy Issuance

Once approved, the policy is formally issued. Documentation is prepared, contracts are generated, and the policyholder receives their coverage details.

Premium Accounting & Customer Servicing

Ongoing tasks include processing payments, handling claims, managing policy changes, and responding to customer inquiries. These tasks repeat continuously throughout the policy term.

Renewals and Updates

As policies approach renewal, servicing teams initiate renewal processes. Policyholders may request coverage updates, address changes, or coverage adjustments—each requiring documentation and system updates.

Key Challenges in Policy Administration

Why do insurance companies struggle with policy administration? The answer lies in volume, complexity, and resource constraints.

Why Outsource Insurance Policy Administration?

Insurance policy processing is one of the most operationally intensive tasks within insurance organizations. Outsourcing transfers these labor-intensive functions to dedicated service providers who specialize in managing them.

Cost Efficiency

Outsourcing reduces payroll overhead, eliminates the cost of recruiting and training staff, and avoids the expense of maintaining infrastructure. Providers achieve economies of scale by handling policies for multiple clients.

Operational Efficiency

Outsourcing partners use standardized processes and technology platforms optimized for policy administration. Tasks are completed faster with fewer errors. Organizations like Strada report answering 85%+ of calls and providing 24/7/365 availability, ensuring workflows keep moving smoothly.

Focus on Core Business

Internal teams can redirect their attention to sales, underwriting, customer relationships, and strategic growth instead of routine administrative work. This shift improves overall business performance.

Scalability

As policy volumes fluctuate, outsourcing partners scale resources up or down. Companies avoid the fixed cost of maintaining a large internal team during slow periods.

Compliance and Risk Management

According to the Department of Labor, outsourcing employee benefit plan services allows plan sponsors to gain access to expertise and technology while maintaining oversight. Outsourcing partners stay current with regulatory changes and implement controls to minimize compliance risk.

Types of Tasks to Outsource

Not all policy administration functions need outsourcing. Here's what typically makes sense to delegate:

- Data Entry and Processing: Converting application forms into system records

- Documentation: Preparing policies, contracts, and correspondence

- Premium Accounting: Processing payments, managing billing cycles, reconciling accounts

- Customer Support: Answering routine inquiries, processing address changes, handling service requests

- Claims Support: Managing claim documentation and initial claim processing

- Renewals Administration: Generating renewal notices, processing renewal applications

Functions that typically remain internal include underwriting decisions, claims approval authority, and strategic policy management.

Choosing the Right Outsourcing Partner

Not all outsourcing providers are equal. Here's what to do:

- Take time to ask detailed questions.

- Request references from current clients in your segment.

- Understand their technology stack and how it integrates with yours.

- Verify certifications and compliance credentials.

Add Policy Administration Support with NeoWork

Insurance policy administration outsourcing can help insurers manage routine customer and back-office work without overloading internal teams. NeoWork supports insurance operations through staffing and operational support, including customer experience management, administrative support, claims processing, compliance support, and policy support. Their 91% annualized teammate retention rate and 3.2% candidate selectivity rate are especially useful for policy administration because support teams need to understand internal processes, customer expectations, and recurring documentation requirements.

Policy administration tasks NeoWork can provide:

- policy information and documentation support

- billing-related admin and follow-ups

- claims, compliance, and back-office support

👉Contact NeoWork to add policy administration support that keeps routine insurance workflows organized, improves customer response consistency, and reduces pressure on internal teams.

Outsourcing Models: Onshore vs. Offshore

Two primary outsourcing approaches exist, each with trade-offs:

Many insurers use hybrid models—combining onshore account management with offshore processing to balance costs and control.

Best Practices for Successful Outsourcing

Successful outsourcing requires more than just selecting a vendor. Here's what works:

Clear Scope Definition

Define exactly what work is being outsourced, including volume expectations, quality standards, and timelines. Ambiguity leads to disputes and poor outcomes.

Strong Service Level Agreements

Establish measurable SLAs covering turnaround times, accuracy rates, availability, and escalation procedures. These protect your business and provide accountability.

Ongoing Monitoring

Don't hand off work and disappear. Monitor quality, volume, compliance, and cost metrics regularly. Schedule reviews with the partner to discuss performance and improvement opportunities.

Secure Knowledge Transfer

Invest time in training the outsourcing team on your policies, procedures, systems, and business requirements. Poor knowledge transfer is a leading cause of outsourcing failure.

Maintain Internal Oversight

As noted by the SEC's guidance on outsourcing by investment advisers, organizations cannot waive their fiduciary duty. The organization must oversee outsourced functions to ensure legal obligations are met, regardless of who performs the work.

Common Outsourcing Pitfalls

But wait—outsourcing isn't without risk. Watch out for these common mistakes:

- Choosing Solely on Price: The cheapest option often delivers the poorest quality, creating expensive problems later

- Inadequate Due Diligence: Failing to verify provider credentials, capabilities, and stability exposes your business to operational risk

- Poor Communication: Unclear expectations and infrequent check-ins lead to misalignment and mistakes

- Losing Control: Over-delegating without maintaining oversight violates fiduciary responsibilities and creates compliance exposure

- Rapid Scaling: Growing volumes too quickly without adequate quality controls overwhelms the partner and degrades service

Conclusion

Insurance policy administration outsourcing isn't a one-size-fits-all solution. But for carriers, MGAs, wholesalers, and agencies drowning in administrative work, it's a practical way to reduce costs, improve efficiency, and refocus energy on business growth.

Success requires careful partner selection, clear contractual terms, ongoing monitoring, and maintained internal oversight. The investment in proper outsourcing governance pays dividends through improved operations and reduced compliance risk.

Ready to evaluate outsourcing for your organization? Start by documenting your current processes, estimating volumes and costs, and identifying which tasks are candidates for delegation. Then request proposals from qualified providers and compare their capabilities, pricing, and fit for your business.

Frequently Asked Questions

Topics

Related Blogs

Related Podcasts