.avif)

.avif)

Insurance Staffing Outsourcing Guide 2026

Quick Summary: Insurance staffing outsourcing involves delegating recruitment, training, and management of insurance professionals to specialized third-party providers. This guide covers assessment strategies, outsourcing models, implementation steps, and how to maximize efficiency while maintaining quality control and operational compliance.

What Is Insurance Staffing Outsourcing?

Insurance staffing outsourcing means contracting external providers to handle recruitment, onboarding, and day-to-day management of insurance professionals. Rather than building these capabilities in-house, insurers and agencies partner with specialized firms that understand the industry's unique demands.

The shift toward outsourcing reflects a broader challenge: insurance operations rarely fail because teams don't care. They break when volume spikes, workflows aren't standardized, and hiring can't keep pace. Outsourcing addresses all three.

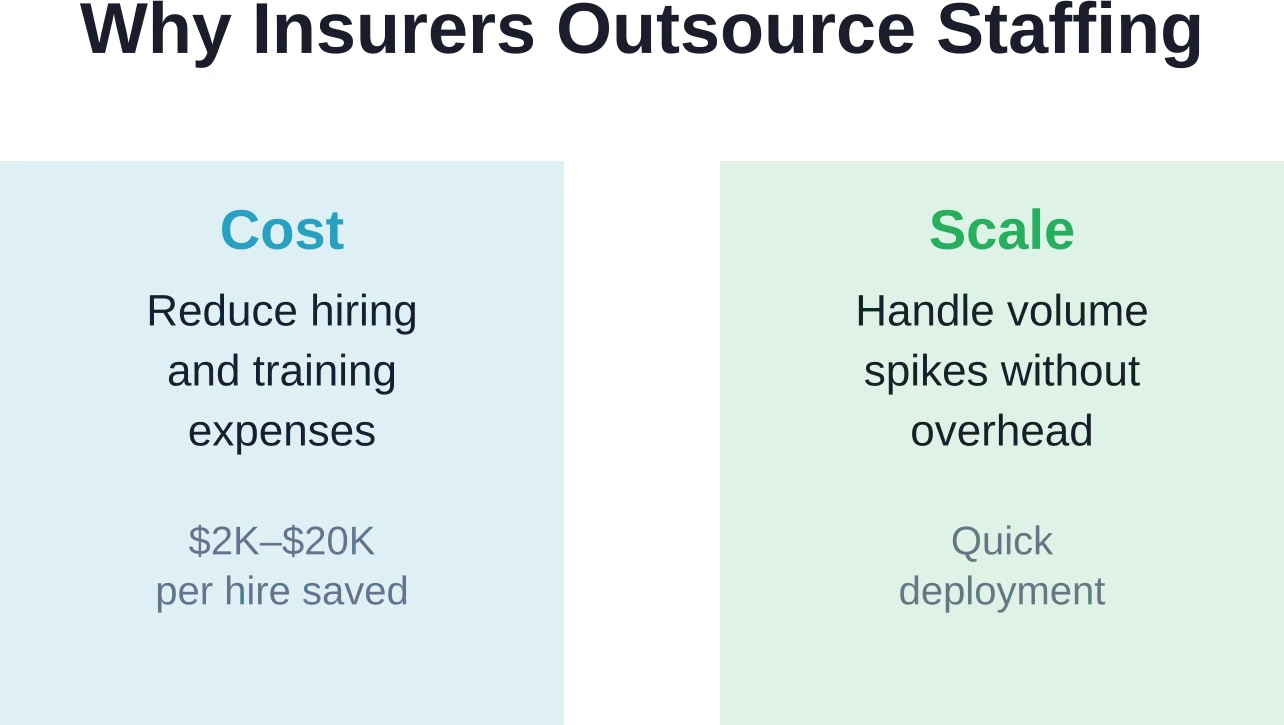

Why Insurance Companies Are Turning to Outsourcing

Hiring remains expensive and time-consuming. According to industry reports, companies can spend anywhere from $2,000 to $20,000 to recruit and onboard a single employee, depending on role and location. Beyond direct costs, lost productivity during recruitment and training compounds the financial burden.

Additionally, insurance operations face mounting pressure from regulatory scrutiny, rising loss ratios, new digital-first competitors, and customer expectations for around-the-clock support. These forces make scaling internal teams impractical. McKinsey research suggests that insurers can improve productivity and reduce operational expenses by up to 40 percent over the next decade by reimagining processes—and outsourcing plays a central role in that transformation.

Key Staffing Processes You Can Outsource

Not all insurance functions require outsourcing. Strategic outsourcing focuses on specific, high-volume, or specialized areas that consume resources disproportionately.

Claims Processing and Adjudication

Claims processing is labor-intensive and seasonal. Outsourced teams handle intake, document review, eligibility verification, and initial adjudication. This reduces claims cycle time and improves customer satisfaction without requiring permanent headcount increases.

Customer Service and Support

Contact centers represent a significant operational cost. Policy inquiries, billing questions, and complaint resolution can be handled by external partners trained in insurance operations and compliance requirements.

Underwriting Support and Policy Administration

Administrative underwriting, document collection, application processing, and policy servicing are prime candidates for outsourcing. These roles don't require senior expertise but do require attention to detail and process adherence.

Managing General Agency Services

MGAs and wholesalers often outsource agency management functions. Per-policy fee arrangements (typically around $25 per policy) make outsourcing economically viable at scale.

Outsourcing Models and Approaches

Different outsourcing models suit different organizational needs. Understanding each helps identify the best fit.

Assessing Your Insurance Staffing Needs

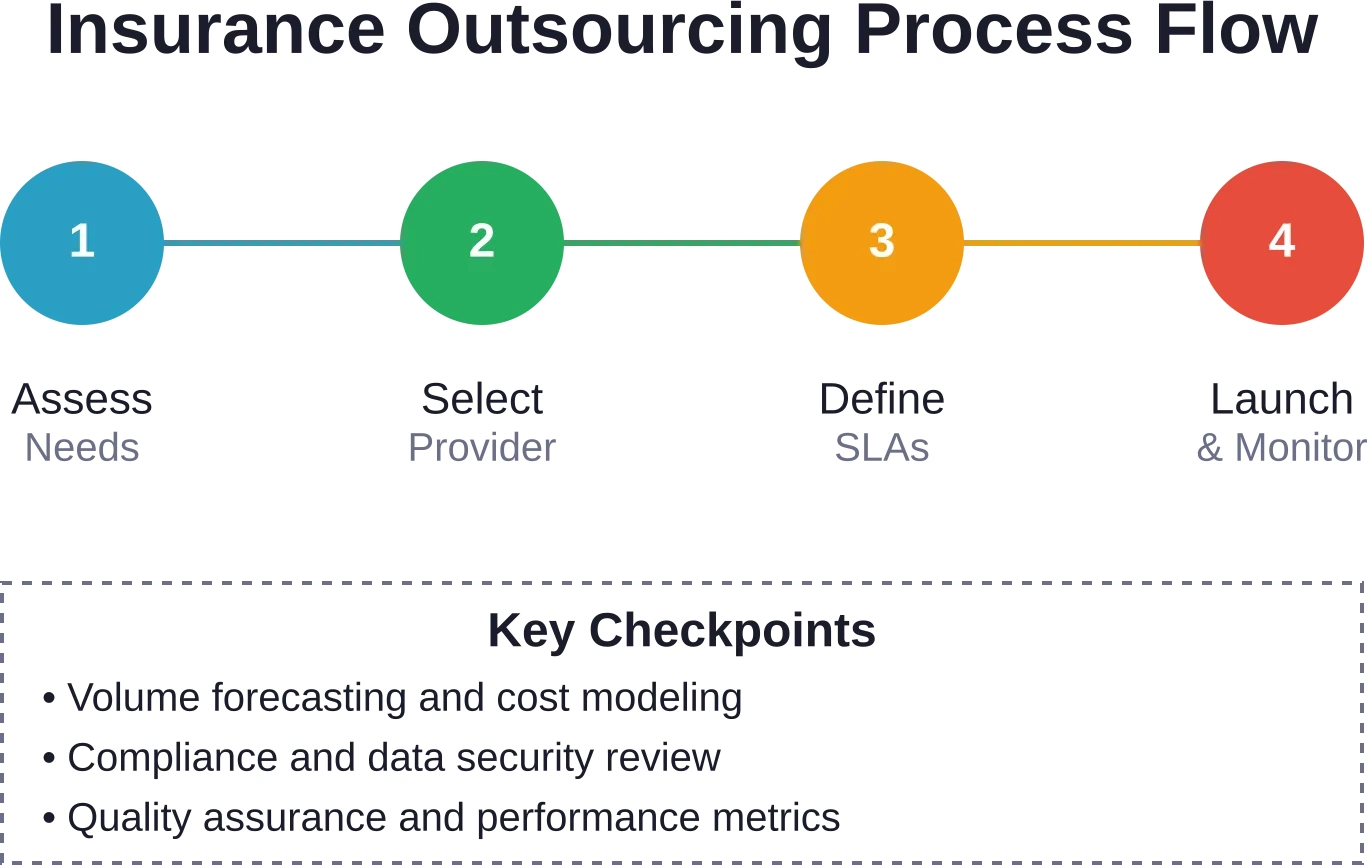

Before outsourcing, determine what actually needs to be outsourced. Start by mapping your current operation: which processes consume the most labor? Where do errors occur most frequently? Which areas face seasonal or unpredictable volume swings?

Cost-benefit analysis is essential. Calculate current hiring costs, training expenses, turnover, and lost productivity. Compare that total against outsourcing fees, transition costs, and management overhead. Use structured assessment frameworks from resources like Harvard Business School to ensure objectivity.

Next, identify skill requirements and compliance constraints. Insurance roles often demand specific licensing (adjuster licenses, insurance agent credentials) or regulatory knowledge. External providers should already have these capabilities.

How to Choose an Insurance Outsourcing Partner

Vendor selection determines success or failure. Look for providers with demonstrable insurance industry experience. They should understand underwriting workflows, claims processes, regulatory requirements, and customer service standards specific to insurance.

Evaluate their infrastructure for data security and compliance. Insurance data triggers HIPAA, state insurance regulations, and security standards. Ask about certifications, audit trails, and incident response protocols.

Check references from other insurers or agencies they serve. Ask specific questions: How did they handle volume spikes? What was their quality performance? How responsive is their management to operational changes?

Service level agreements (SLAs) should be explicit. Include metrics for turnaround time, accuracy rates, customer satisfaction, and escalation procedures. Payment terms typically include a 30-day invoice due date with 12% annual interest on undisputed unpaid charges.

Add Insurance Staffing Support with NeoWork

Insurance staffing outsourcing works best when companies need reliable people for recurring customer, claims, compliance, policy, and administrative workflows. NeoWork supports insurance operations through dedicated offshore staffing, with roles that can fit into existing processes instead of replacing the company’s internal decision-making. The company reports a 91% annualized teammate retention rate and a 3.2% candidate selectivity rate, which is useful when insurance teams need people who can learn procedures, handle repetitive work carefully, and stay consistent over time.

Insurance staffing roles NeoWork can provide you with:

- insurance claims processing staff

- administrative and documentation support

- compliance, claims, and policy support workflows

Contact NeoWork to build insurance staffing support that helps manage recurring operational work, improves process continuity, and reduces pressure on internal teams.

Implementation and Transition Strategy

Successful transitions require careful planning. Start with a pilot program on one small process or team rather than a full cutover. Pilot phases typically last 60–90 days.

During transition, establish clear workflows, documentation standards, and quality checkpoints. The service provider should remediate rejected acceptance items within 7 business days. Build in acceptance testing and sign-off gates before moving volumes into production.

Staff your internal team for oversight and relationship management, not transaction handling. Someone needs to monitor SLAs, escalate problems, and manage provider communication. Outsourcing reduces labor but doesn't eliminate internal coordination.

Maintaining Control and Quality

Outsourcing doesn't mean losing visibility. Implement real-time dashboards tracking volume, turnaround time, accuracy, and quality metrics. Regular audits—at least quarterly—catch issues before they become systemic.

Change management can get complex. If your operation volume grows during renewal season, most agreements allow up to a 25% increase in accounts or items processed without renegotiation. Beyond that threshold, fee adjustments apply. Plan for this in advance.

Build escalation procedures into your SLA. What happens if the provider misses performance targets? Can you shift work back in-house? Are there financial penalties? Clear escalation paths prevent disputes later.

Common Pitfalls to Avoid

Setting unrealistic expectations tops the list. Outsourcing improves efficiency but won't magically fix broken processes. If workflows are undefined internally, outsourcing them doesn't clarify them—it just confuses someone else's problem.

Poor communication during transition often derails implementations. Ensure your internal team and the outsourcing partner align on procedures, compliance requirements, and quality standards before day one.

Underestimating data security risks is dangerous. Failing to deliver required employee certifications can trigger default fines of up to 10% of annual service fees. Ensure the provider has robust identity verification and credential management.

Conclusion

Insurance staffing outsourcing isn't a shortcut—it's a strategic lever for cost control, scalability, and operational flexibility. When done right, outsourcing lets insurers and agencies focus internal resources on high-value work: underwriting judgment, customer relationships, and business development.

The decision hinges on an honest assessment of your current operation: which processes drain resources disproportionately? Where can external expertise add value? Start with a clear pilot, measure results objectively, and build the relationship carefully.

The insurers gaining the most traction with outsourcing aren't the ones trying to cut costs at any expense. They're the ones using outsourcing to unlock growth—handling volume spikes, expanding into new markets, and delivering better customer service without expanding headcount. That's the real opportunity in this space.

FAQ: Insurance Staffing Outsourcing

Topics

Insurance Staffing Outsourcing Guide 2026

Quick Summary: Insurance staffing outsourcing involves delegating recruitment, training, and management of insurance professionals to specialized third-party providers. This guide covers assessment strategies, outsourcing models, implementation steps, and how to maximize efficiency while maintaining quality control and operational compliance.

What Is Insurance Staffing Outsourcing?

Insurance staffing outsourcing means contracting external providers to handle recruitment, onboarding, and day-to-day management of insurance professionals. Rather than building these capabilities in-house, insurers and agencies partner with specialized firms that understand the industry's unique demands.

The shift toward outsourcing reflects a broader challenge: insurance operations rarely fail because teams don't care. They break when volume spikes, workflows aren't standardized, and hiring can't keep pace. Outsourcing addresses all three.

Why Insurance Companies Are Turning to Outsourcing

Hiring remains expensive and time-consuming. According to industry reports, companies can spend anywhere from $2,000 to $20,000 to recruit and onboard a single employee, depending on role and location. Beyond direct costs, lost productivity during recruitment and training compounds the financial burden.

Additionally, insurance operations face mounting pressure from regulatory scrutiny, rising loss ratios, new digital-first competitors, and customer expectations for around-the-clock support. These forces make scaling internal teams impractical. McKinsey research suggests that insurers can improve productivity and reduce operational expenses by up to 40 percent over the next decade by reimagining processes—and outsourcing plays a central role in that transformation.

Key Staffing Processes You Can Outsource

Not all insurance functions require outsourcing. Strategic outsourcing focuses on specific, high-volume, or specialized areas that consume resources disproportionately.

Claims Processing and Adjudication

Claims processing is labor-intensive and seasonal. Outsourced teams handle intake, document review, eligibility verification, and initial adjudication. This reduces claims cycle time and improves customer satisfaction without requiring permanent headcount increases.

Customer Service and Support

Contact centers represent a significant operational cost. Policy inquiries, billing questions, and complaint resolution can be handled by external partners trained in insurance operations and compliance requirements.

Underwriting Support and Policy Administration

Administrative underwriting, document collection, application processing, and policy servicing are prime candidates for outsourcing. These roles don't require senior expertise but do require attention to detail and process adherence.

Managing General Agency Services

MGAs and wholesalers often outsource agency management functions. Per-policy fee arrangements (typically around $25 per policy) make outsourcing economically viable at scale.

Outsourcing Models and Approaches

Different outsourcing models suit different organizational needs. Understanding each helps identify the best fit.

Assessing Your Insurance Staffing Needs

Before outsourcing, determine what actually needs to be outsourced. Start by mapping your current operation: which processes consume the most labor? Where do errors occur most frequently? Which areas face seasonal or unpredictable volume swings?

Cost-benefit analysis is essential. Calculate current hiring costs, training expenses, turnover, and lost productivity. Compare that total against outsourcing fees, transition costs, and management overhead. Use structured assessment frameworks from resources like Harvard Business School to ensure objectivity.

Next, identify skill requirements and compliance constraints. Insurance roles often demand specific licensing (adjuster licenses, insurance agent credentials) or regulatory knowledge. External providers should already have these capabilities.

How to Choose an Insurance Outsourcing Partner

Vendor selection determines success or failure. Look for providers with demonstrable insurance industry experience. They should understand underwriting workflows, claims processes, regulatory requirements, and customer service standards specific to insurance.

Evaluate their infrastructure for data security and compliance. Insurance data triggers HIPAA, state insurance regulations, and security standards. Ask about certifications, audit trails, and incident response protocols.

Check references from other insurers or agencies they serve. Ask specific questions: How did they handle volume spikes? What was their quality performance? How responsive is their management to operational changes?

Service level agreements (SLAs) should be explicit. Include metrics for turnaround time, accuracy rates, customer satisfaction, and escalation procedures. Payment terms typically include a 30-day invoice due date with 12% annual interest on undisputed unpaid charges.

Add Insurance Staffing Support with NeoWork

Insurance staffing outsourcing works best when companies need reliable people for recurring customer, claims, compliance, policy, and administrative workflows. NeoWork supports insurance operations through dedicated offshore staffing, with roles that can fit into existing processes instead of replacing the company’s internal decision-making. The company reports a 91% annualized teammate retention rate and a 3.2% candidate selectivity rate, which is useful when insurance teams need people who can learn procedures, handle repetitive work carefully, and stay consistent over time.

Insurance staffing roles NeoWork can provide you with:

- insurance claims processing staff

- administrative and documentation support

- compliance, claims, and policy support workflows

Contact NeoWork to build insurance staffing support that helps manage recurring operational work, improves process continuity, and reduces pressure on internal teams.

Implementation and Transition Strategy

Successful transitions require careful planning. Start with a pilot program on one small process or team rather than a full cutover. Pilot phases typically last 60–90 days.

During transition, establish clear workflows, documentation standards, and quality checkpoints. The service provider should remediate rejected acceptance items within 7 business days. Build in acceptance testing and sign-off gates before moving volumes into production.

Staff your internal team for oversight and relationship management, not transaction handling. Someone needs to monitor SLAs, escalate problems, and manage provider communication. Outsourcing reduces labor but doesn't eliminate internal coordination.

Maintaining Control and Quality

Outsourcing doesn't mean losing visibility. Implement real-time dashboards tracking volume, turnaround time, accuracy, and quality metrics. Regular audits—at least quarterly—catch issues before they become systemic.

Change management can get complex. If your operation volume grows during renewal season, most agreements allow up to a 25% increase in accounts or items processed without renegotiation. Beyond that threshold, fee adjustments apply. Plan for this in advance.

Build escalation procedures into your SLA. What happens if the provider misses performance targets? Can you shift work back in-house? Are there financial penalties? Clear escalation paths prevent disputes later.

Common Pitfalls to Avoid

Setting unrealistic expectations tops the list. Outsourcing improves efficiency but won't magically fix broken processes. If workflows are undefined internally, outsourcing them doesn't clarify them—it just confuses someone else's problem.

Poor communication during transition often derails implementations. Ensure your internal team and the outsourcing partner align on procedures, compliance requirements, and quality standards before day one.

Underestimating data security risks is dangerous. Failing to deliver required employee certifications can trigger default fines of up to 10% of annual service fees. Ensure the provider has robust identity verification and credential management.

Conclusion

Insurance staffing outsourcing isn't a shortcut—it's a strategic lever for cost control, scalability, and operational flexibility. When done right, outsourcing lets insurers and agencies focus internal resources on high-value work: underwriting judgment, customer relationships, and business development.

The decision hinges on an honest assessment of your current operation: which processes drain resources disproportionately? Where can external expertise add value? Start with a clear pilot, measure results objectively, and build the relationship carefully.

The insurers gaining the most traction with outsourcing aren't the ones trying to cut costs at any expense. They're the ones using outsourcing to unlock growth—handling volume spikes, expanding into new markets, and delivering better customer service without expanding headcount. That's the real opportunity in this space.

FAQ: Insurance Staffing Outsourcing

Topics

Related Blogs

Related Podcasts